The quickest way to find the right personal loan is to stop looking for a “perfect” rate and start looking for a term that doesn’t choke your monthly cash flow. You need to match the loan’s structure to your specific reason for borrowing, whether that is a sudden car repair or a long-term home improvement project.

Most people approach debt as a monolithic beast, a single scary concept that looms over their bank statements like a dark cloud, but in reality, the market is a fragmented mess of different products designed for very different financial personalities. You have the high-speed digital lenders, the old-school institutional giants, and the niche Shari’a-compliant options that exist specifically to accommodate different cultural and religious requirements.

If you are looking at a pile of brochures, you will quickly realize that the “lowest rate” is often a ghost. It looks real in the fine print, but once you factor in the origination fees, the prepayment penalties, and the actual duration of the repayment, that 4% might actually cost you more than a 5.5% loan with no hidden exit fees. It is a game of math, not marketing.

Take the current offerings in the European market as a baseline. If you are a client of a major bank and you need to bridge a gap for a specific purchase, you might look at online personal loans at a 5.00% fixed interest rate, which provides a level of predictability that variable rates simply cannot offer when the central banks decide to change their stance.

Predictability is your best friend when you are trying to sleep at night. A fixed rate means you know exactly what your outgoing payment will be in month thirty-six, regardless of what happens to inflation or global supply chains. This certainty is worth a slight premium in some cases, but it prevents the sudden, nauseating shock of a monthly payment jumping by a hundred dollars because a central banker decided to tighten the money supply.

Deciphering the Fine Print of Repayment Terms

Time is the most expensive ingredient in any loan agreement. The longer you take to pay it back, the less you pay each month, but the more you end up paying the bank in total interest. It is a classic trade-off that feels like a lose-lose scenario if you do not have a plan. You might find yourself staring at a five-year term and realizing that your “cheap” monthly payment is actually a slow leak in your long-term wealth.

Consider the options available in the Middle East, where the structure of the loan often depends heavily on your current employment status and banking relationship. For instance, anb offers competitive low rates with repayment terms up to 5 years, which is a standard window for most unsecured personal financing. This five-year limit is common because it provides enough time to make the monthly installments manageable without the total interest cost spiraling completely out of control.

Then there is the specialized niche of Shari’a-compliant finance, which operates under different principles than traditional interest-bearing loans. If you want to avoid the concept of interest entirely, you might look at something like the Riyad Bank option for financing without salary transfer, which allows for repayment over up to 60 months. This is a significant advantage if you work for a company that doesn’t have a direct payroll link to your primary bank, providing a level of flexibility that many traditional lenders refuse to budge on.

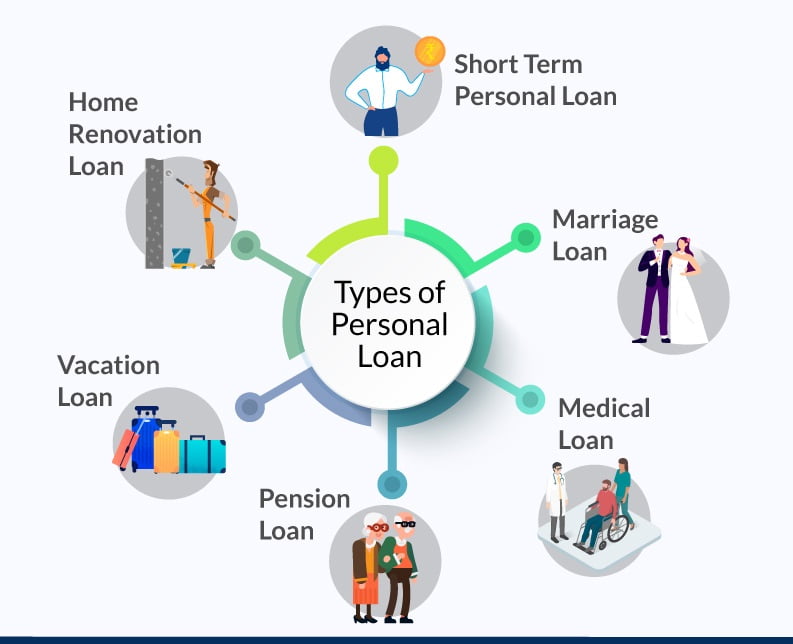

You should also be aware of how “unsecured” status affects your options. A collateral-free loan is essentially a loan based on your reputation and your income, which is why the interest rates are higher than a mortgage. If you are looking at HDB Financial Services, you will see that they focus on quick, hassle-free, and collateral-free options, which is ideal for someone who needs cash for a specific purpose, like a wedding or a medical bill, but doesn’t want to risk their car or their house to get it.

When comparing these services, you should keep a spreadsheet of these specific variables:

- Total cost of credit (the sum of all payments, not just the principal).

- Prepayment penalties (the fee you pay if you decide to pay the loan off early).

- Origination fees (the “entry ticket” cost that is often deducted from your payout).

- The “Effective Interest Rate” vs. the “Nominal Interest Rate.”

It is easy to get distracted by a low monthly payment. A loan for $10,000 over three years is much easier to swallow than a loan for $10,000 over seven years, but the math tells a different story. If you can afford the higher monthly payment, take the shorter term. It is the only way to truly win the game against the lender.

The Hidden Mechanics of Credit Assessment

Lenders do not just look at your salary; they look at your life. They want to know if you are the kind of person who spends 60% of your income on rent and dining out, or if you are someone who lives within your means. They use algorithms to predict how likely you are to miss a payment, and these algorithms are often surprisingly sensitive to small changes in your financial behavior.

If you are applying through a major UK provider like Novuna Personal Finance, you are dealing with a company that has been in the market for over 40 years. These types of established firms have seen every possible type of borrower, from the person who is perfectly solvent but has a weird credit history to the person who is a high earner but manages their debt poorly. They are not looking for reasons to say yes; they are looking for any reason to say no.

This is why your “Brand Anchors” and your credit score matter more than any sales pitch. You might think your income is the most important factor, but for many lenders, the ratio of your existing debt to your income is the real deciding factor. If you are already carrying three credit cards and a car loan, a new personal loan becomes a much harder sell, regardless of how much you earn. They see the debt-to-income ratio as a measure of your breathing room.

I once knew a guy, a high-flying architect with a massive salary, who applied for a small $5,000 loan to renovate his home office and was rejected immediately because he had recently opened a new retail credit line for a high-end espresso machine. The bank saw the “new inquiry” and the sudden increase in his available credit as a sign of potential distress. One small purchase can derail a large loan application if the timing is wrong.

You need to time your applications carefully. If you are planning to apply for a mortgage in six months, do not go around applying for personal loans to fund a vacation or a new TV. Every time you apply, it leaves a footprint on your credit report. Too many footprints in a short period make you look desperate, and desperate people are high-risk borrowers in the eyes of a computer program.

Comparing Market Realities and Regional Differences

Geography dictates your options. If you are in Malaysia, you might find that private sector financing has a different flavor entirely, with providers like Bank Rakyat offering products specifically tailored to the private sector with competitive profit rates. The term “profit rate” instead of “interest rate” is a subtle but important distinction in Islamic finance, reflecting a different underlying mechanism for how the cost of borrowing is structured.

It is a strange world where a person in London has a completely different set of tools and regulatory protections than someone in Riyadh or Kuala Lumpur. You have to understand the local landscape before you even begin to look at numbers. An interest rate that seems low in one country might be standard in another, and the rules regarding how much you can borrow relative to your salary vary wildly across borders.

To help you visualize the differences, look at how these providers approach the user experience and their core value proposition:

| Provider Type | Primary Benefit | Typical Target Audience |

|---|---|---|

| Digital-First Apps | Speed and convenience | Younger users with straightforward credit |

| Traditional Banks | Established trust and bundled services | Existing bank clients with stable histories |

| Specialized Finance | Niche products (e.g., Shari’a-compliant) | Users with specific cultural or employment needs |

| Unsecured Specialists | No collateral required | People needing quick liquidity for personal use |

Don’t let the glossy websites fool you into thinking the process is always “seamless.” Most of these digital applications are actually quite rigorous. You will be asked to upload bank statements, proof of identity, and proof of income, and if there is even a single discrepancy between your stated income and what your bank statements show, the whole process can grind to a halt. Accuracy is more important than speed when you are filling out these forms.

You should also consider the psychological weight of the debt. Borrowing for an asset that holds value, like a car or a home improvement project, feels different than borrowing for a lifestyle purchase, like a high-end watch or a luxury holiday. The former is an investment in your standard of living, while the latter is simply an acceleration of your spending. The math might be the same, but the long-term impact on your net worth is not.

If you are skeptical about whether any of this is worth the hassle, remember that a well-timed, well-managed loan is simply a tool that allows you to move your future wealth into the present, and if you use it to fund an asset or a necessary expense rather than a temporary luxury, it is a strategic move rather than a financial mistake. If you want to go deeper, Brand Anchors is a solid place to start.

Good to know

What is the difference between a personal loan and a line of credit?

A personal loan provides a lump sum of cash upfront with a fixed repayment schedule, while a line of credit allows you to draw funds as needed up to a specific limit.

How does my credit score affect my loan interest rate?

A higher credit score indicates lower risk to lenders, typically qualifying you for lower interest rates and better loan terms.

What are the most common requirements for qualifying for personal financing?

Lenders typically require proof of identity, steady income verification, a stable employment history, and a sufficient credit score.

Are there penalties for paying off a loan early?

Some loans include prepayment penalties, so it is essential to check your specific loan agreement for any fees associated with early repayment.

What should I consider before taking out a personal loan?

Evaluate the total cost of borrowing including interest rates, monthly payment affordability, and whether the loan is necessary for debt consolidation or an emergency.